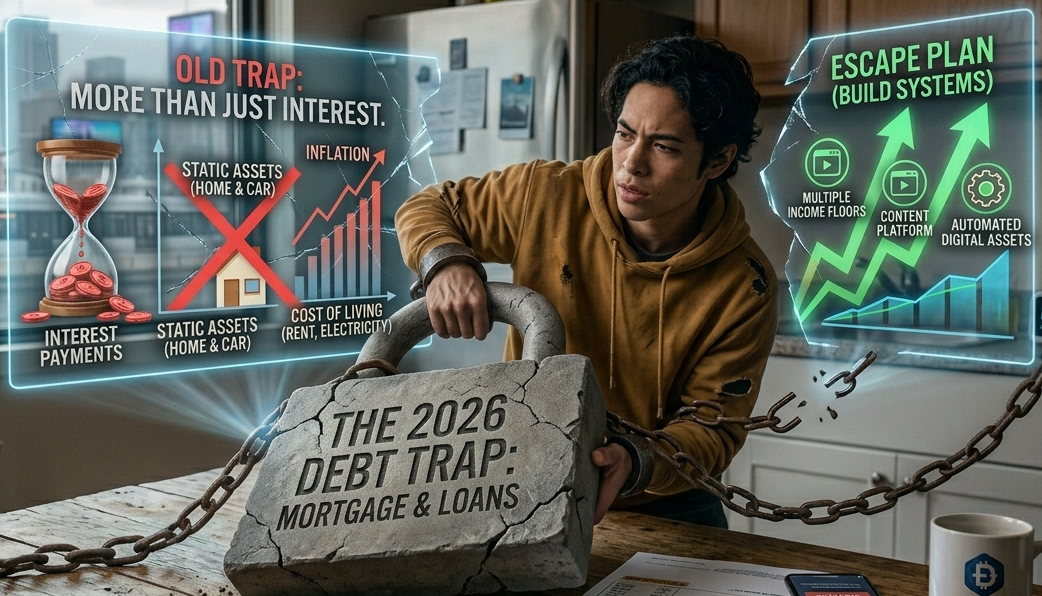

In 2026, the traditional understanding of debt is being dismantled. Most people look at their mortgage, car loan, or line of credit and see a simple mathematical equation where the principal plus the interest rate equals the cost of the debt. This view is naive. If you are calculating the cost of your debt based solely on your interest rate, you are missing the most expensive components of your financial obligation and falling into the 2026 debt trap.

The Hidden Cost of Opportunity

The real cost of your debt is not what you pay to the bank, but rather what you cannot do with the money you are forced to pay them. Every dollar that goes toward a monthly loan payment is a dollar that cannot be invested into high-yield digital assets or automated systems. When you carry long-term debt, you are effectively handicapping your ability to pivot in an economy that demands speed and adaptability. You are paying a hidden freedom tax every month. While others are using their capital to build scalable income streams, you are using yours to secure a static asset that is likely depreciating or yielding minimal returns.

The Inflationary Mirage

Many believe that inflation helps those in debt because the value of the money they pay back decreases over time, but this is an inflationary mirage. In 2026, while the value of the currency may shift, the cost of living is rising much faster than the value of stagnant assets. If your debt is tied to an asset that is not actively generating income, you are losing on two fronts because you are paying interest to a lender while simultaneously losing the purchasing power that those payments represented. You are not just losing money, but you are losing the ability to compete in the current marketplace.

Liability Versus Asset

There is a massive distinction between good debt and bad debt, yet most people confuse the two. In the modern economy, any debt that does not directly fund a system capable of producing its own revenue is a pure liability. If your loan funds a lifestyle such as a house, a car, or consumer goods, you are not building equity but rather a cage. The moment your income fluctuates or the market demands a new skill set, your debt becomes an anchor that prevents you from making the necessary moves.

Escaping the Trap

To survive and thrive in 2026, you need to change your relationship with debt starting by auditing your obligations to categorize every debt based on whether it is generating cash flow or consuming it. You should also prioritize liquidity because in the current economic climate, cash flow is king. Before paying off low-interest debt, consider if that capital could be better utilized to build an automated income stream that pays off the debt faster. Finally, shift your mindset to stop viewing debt as a normal part of life and start viewing it as an obstacle to your autonomy.

Conclusion: Reclaim Your Financial Future

The 2026 debt trap is designed to keep you locked into the traditional workforce, fearful of risk, and unable to innovate. It thrives on your compliance and your belief that your payments are just a part of adult life. They are not. They are a systematic extraction of your potential. Stop accepting the cost of your debt as inevitable. Audit your liabilities, eliminate the ones that drain your resources, and start directing your capital toward assets that you own and that work for you. Your freedom is worth more than any convenience your debt has bought you.